Voluntary Health Insurance Scheme (VHIS) is a government-regulated health insurance scheme launched by the Health Bureau in 2019. It aims at providing standardised health insurance protection with greater transparency. All certified plans must meet the government's minimum benefit requirements. These include guaranteed renewal, coverage of unknown pre-existing conditions, and standard benefit items. This makes it easier for consumers to compare plans across different insurers.

Get more informationBupa VHIS — FAQ Page

About VHIS

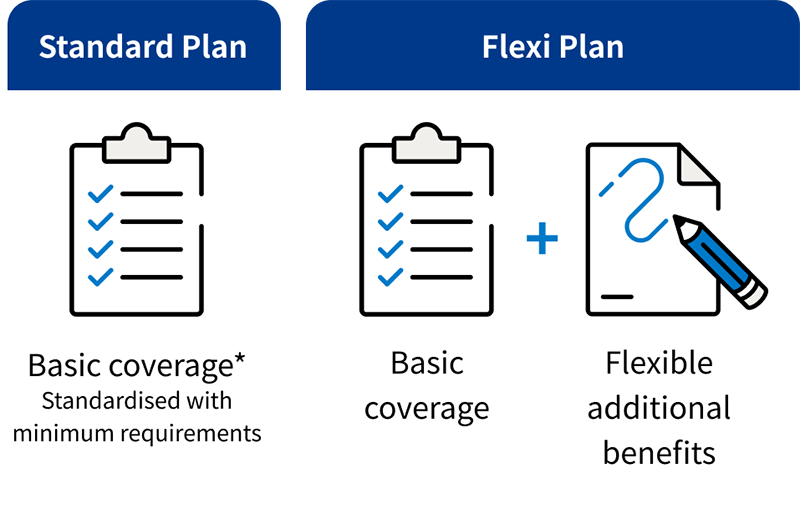

There are two types of VHIS certified plans: the Standard Plan and the Flexi Plan.

Standard Plan

Terms and benefits are fully standardised with minimum requirements, such as a minimum level of coverage and reimbursement.

Flexi Plan

It must include all the basic benefits of a Standard Plan. Insurers can also add flexible optional benefits on top. These are subject to rules set by the Health Bureau.

Consumers can choose the type that best suits their needs.

Standard Plan

Terms and benefits are fully standardised with minimum requirements, such as a minimum level of coverage and reimbursement.

Flexi Plan

It must include all the basic benefits of a Standard Plan. Insurers can also add flexible optional benefits on top. These are subject to rules set by the Health Bureau.

Consumers can choose the type that best suits their needs.

VHIS is suitable for anyone who wants access to private hospital services or more flexible treatment choices. This includes working adults, family members, and those planning ahead for future medical costs. Even if you are insured under a group medical insurance, VHIS can serve as a personal supplement to increase your coverage. It also ensures you stay covered after leaving your employment.

VHIS is a government-certified scheme. All plans must follow standard terms. These include guaranteed renewal up to age 100, coverage of unknown pre-existing conditions, and minimum benefit coverage and reimbursement amounts. Regular medical insurance is designed by individual insurers. Terms and coverage may vary from plan to plan. Consumers should always compare carefully before purchase.

Yes. Under the Inland Revenue Ordinance (Cap. 112), you can claim a tax deduction for VHIS premiums paid for yourself or specified relatives. The maximum deduction is HK$8,000 per insured person per tax year. There is no cap on the number of insured persons. This makes VHIS a practical option for family-wide medical protection and tax planning.

Visit GovHK Tax Deduction

Standard Plan

A waiting period applies only to unknown pre-existing conditions. Reimbursement rate for pre-existing conditions unknown at the time of enrolment is phased over the first three policy years — 0%, 25%, and 50%. You'll receive 100% reimbursement from the 4th policy year onwards. All other benefits for the eligible medical expenses are payable from the policy effective date in accordance with the benefit schedule.

Flexi Plan

The waiting period for unknown pre-existing conditions varies by insurer and certified plan.

Insurers must consider applications from Hong Kong residents aged 15 days to 80 years old. The actual eligible entry age range and premium levels may vary depending on the applicant's age. In general, the younger you enrol, the lower your premium and the simpler the underwriting. Early cover also means more years of protection.

Yes. All certified VHIS plans offer guaranteed renewal up to age 100. As long as you pay your premium on time, your insurer cannot refuse renewal. This applies even if your health changes or you have made previous claims.

Yes. VHIS covers unknown pre-existing conditions. However, a waiting period and phased reimbursement apply. For known or diagnosed conditions, coverage depends on the underwriting outcome and your specific plan terms.

No, it is not mandatory. Whether VHIS is right for you depends on your needs and budget. It can be useful if you want to shorten waiting times, access private medical services, or prepare for future medical expenses. If you mainly rely on public healthcare, you can consider your personal risk tolerance and decide accordingly.

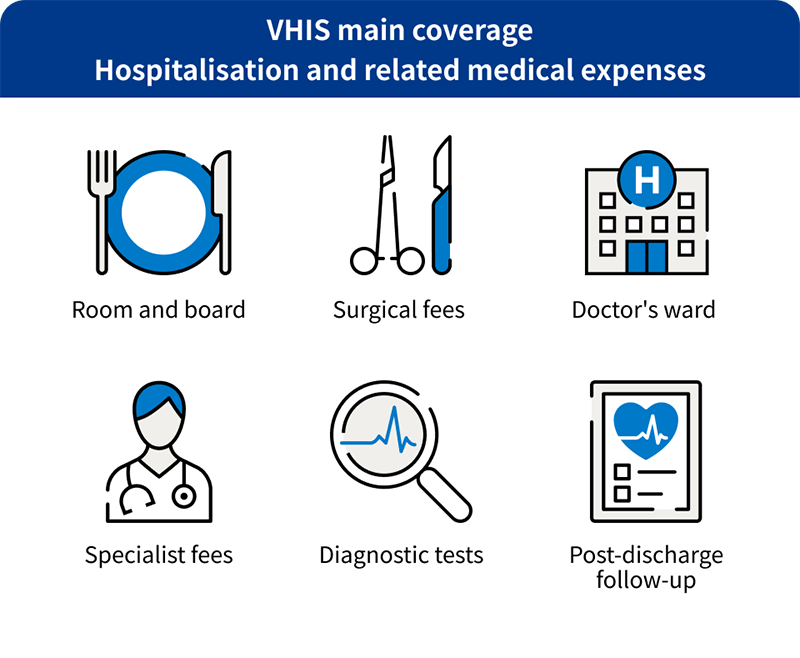

Coverage & Claims

VHIS mainly covers hospitalisation and related medical expenses. This includes

- Room and board

- Surgical fees

- Doctor's ward round fees

- Specialist fees

- Diagnostic tests

- Post-discharge follow-up treatment and more

Benefit limits and coverage vary by plan. Please check the benefit limits and policy terms before you enrol.

The core coverage is focused on inpatient treatment. General outpatient expenses may not be included. Some plans do offer designated outpatient benefits or pre- and post-hospitalisation outpatient cover, such as specialist consultations or follow-up visits. Please check your specific plan for details.

Yes, if the condition was unknown at the time of enrolment. A waiting period and phased reimbursement apply — for example, no payout for the first year, and increasing gradually from the second year onwards. For known or diagnosed conditions, coverage depends on underwriting and your policy terms.

In most cases, no. Conditions diagnosed during the waiting period are either not reimbursed or paid at a lower rate. The waiting period is designed to prevent claims for conditions present before enrolment. We recommend that you enrol early while in good health to minimise restrictions.

Yes. VHIS generally covers inpatient treatment at local private hospitals and eligible medical institutions. Some plans also offer a medical network or direct billing service. This means you may not need to pay the full amount upfront. Please check your plan for details.

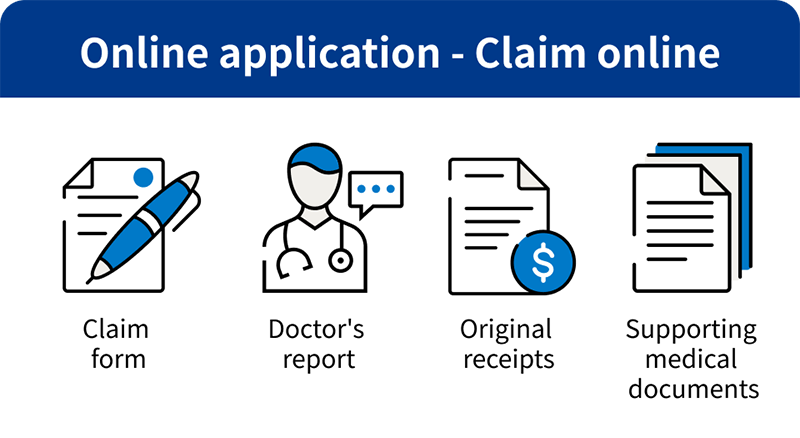

You will need a completed claim form, a doctor's report, original receipts, and relevant medical documents. You can submit your claim online or electronically to speed up processing. We recommend that you find out what documents are required before your admission or treatment.

Processing time depends on the complexity of your case and whether all required documents are complete. In general, it takes a few working days to several weeks. Where the information provided is complete and accurate and meets the requirements set out in the policy terms, it will help speed up the process. If additional medical information is needed, the review may take longer.

The reimbursed amount depends on your policy's benefit limits, actual medical expenses, ward class, and whether a deductible applies. If the medical expenses exceed the plan limit or you have chosen a higher ward class, you may need to pay part of the expenses. Please review your benefit caps before you enrol.

About Bupa VHIS

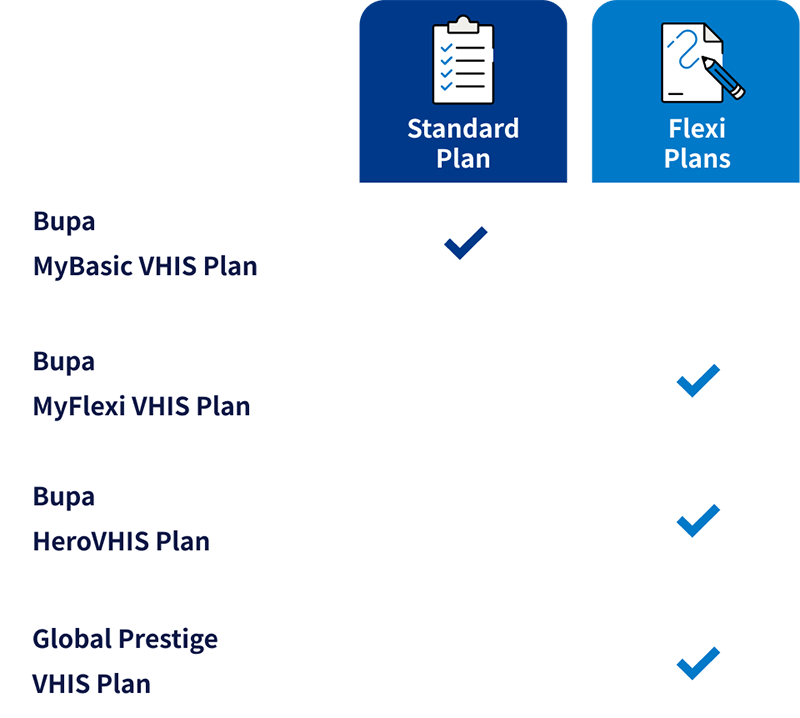

Bupa offers a range of certified VHIS plans to suit different budgets and needs. These include:

Each plan has different benefit amounts, ward classes, and deductible options. You can compare plans based on your needs and budget before subscription.

Discover Bupa VHIS plans now

- Bupa MyBasic VHIS Plan (Standard Plan)

- Bupa MyFlexi VHIS Plan (Flexi Plan)

- Bupa Hero VHIS Plan (Flexi Plan)

- Global Prestige VHIS Plan (Flexi Plan)

Each plan has different benefit amounts, ward classes, and deductible options. You can compare plans based on your needs and budget before subscription.

Discover Bupa VHIS plans now

Yes. All Bupa VHIS plans are certified by the Health Bureau. They meet all relevant minimum benefit requirements. This includes guaranteed lifetime renewal*, coverage of unknown pre-existing conditions^, and standard benefit items. You can trust that your coverage is clear and consistent.

* Bupa guarantees annual renewal for life, subject to the renewal requirements in the Policy Terms and Conditions.

^ Subject to the General Exclusions of the policy

Yes. Some Bupa VHIS Flexi Plans offer multiple deductible options. You can choose a higher or lower deductible to suit your needs. A higher deductible generally means a lower premium. This is a good option if you have group medical insurance or prefer a lower premium paid to use VHIS as a supplemental coverage.

Yes. All certified Bupa VHIS plans offer guaranteed renewal for life*. Pay your premium on time and your insurer will not refuse renewal due to any change in your health or if you have submitted a claim.

* Bupa guarantees annual renewal for life, subject to the renewal requirements in the Policy Terms and Conditions.

Yes. Bupa provides a medical services network. Under certain plans and conditions, cashless service# may be available. This means you may not need to pay in full upfront for treatment. Actual scope of application and arrangement depend on your chosen plan and the medical institution.

# Cashless treatment is not applicable to 1) items (k) and (l) under Basic Benefits, and 2) items (c) to (j) under Enhanced Benefits (if applicable), as listed in the Summary of Benefits of the Certified Plan. Bupa Hero Card is not applicable to outpatient departments of local private hospitals. For overseas treatment, you can enjoy cashless service by contacting Bupa in advance to make the necessary arrangements. Accessing Bupa's cashless service is subject to prescribed procedures and obtain pre-authorisation from Bupa.

Some Bupa VHIS plans provide emergency medical coverage outside Hong Kong; or medical arrangements in designated areas. The scope varies by plan. Please review the geographic coverage and reimbursement terms carefully before you subscribe.

Yes. Health declaration information is normally required when you apply for Bupa VHIS. Our underwriting team will review your declaration. Possible outcomes include standard acceptance, additional premium loading, exclusion of specific conditions, or a request for further medical information.

Yes. You can enrol yourself and eligible family members, including spouse, children, or parents. Each insured person can choose their own plan. This makes it easy to plan family-wide health coverage and maximise tax deductions.

Application & Policy Management

You can apply through our online platform or through a designated channel. You will need to complete your personal details, a health declaration, and select a plan. Once we receive your application and first premium payment, our team will conduct underwriting and confirm your policy effective date.

Get a quote

Underwriting typically takes a few working days. This depends on your health condition and the documents you submit. If your health declaration involves special circumstances, we may need additional medical reports. This can extend the processing time.

Your policy takes effect after your application is approved and first premium payment is received. The exact effective date will be shown in your policy document. Note that some benefits may have a waiting period. Please read your policy terms carefully after subscription.

Yes. You can use our online platform or Blua Health mobile app to view your policy details, coverage, and claims history anytime. You can also update your contact information and manage selected policy services through the app.

Download Blua Health

You can update your address, phone number, or other details through the Blua Health app or by contacting our Customer Service team

- +852 2517 5333 (Individual members)

- +852 2517 5383 (Bupa Gold members)

- +852 2517 5388 (Group members)

Some changes, such as adjusting your coverage level or plan, may require a new application or an underwriting review.

VHIS renews on an annual basis. You can pay by autopay, credit card, or other designated payment methods. Pay on time to keep your policy active and your guaranteed renewal intact.